Investment property loans for doctors are structured differently from standard loans because medical income, career progression, and lending policy don’t always align cleanly. Doctors have unique financial circumstances and career stability, which influence how lenders assess their applications.

- Higher borrowing potential (if structured correctly)

- Flexible lender policies for medical professionals

- Complex income requires tailored assessment

- The medical profession qualifies for tailored loan options

- Poor structure can limit future purchases

Understanding the right loan options is crucial for doctors to maximize their investment potential.

We’ve worked with doctors who could borrow significantly more than they realised… and others who were unintentionally capped after their first purchase. The difference usually comes down to structure, not income.

TL;DR

Investment property loans for doctors are designed to account for high but often complex income, including contractor earnings, private billing, and career progression. While lenders may offer preferential treatment to medical professionals, borrowing capacity is still affected by serviceability buffers, income consistency, and loan structure; choosing the right loan options and structure helps doctors achieve their financial goals and investment goals. The right approach allows doctors to maximise borrowing, preserve flexibility, and scale into multiple properties over time, rather than getting stuck after their first investment.

Why investment property loans for doctors are different from standard loans

On the surface, lending to doctors should be straightforward.

Strong income. Stable career. Low default risk. A doctor’s financial situation and financial circumstances are key factors in lender assessments, as banks tailor mortgage offerings based on these aspects. Demonstrating financial stability through documentation can significantly improve a doctor’s chances of loan approval and securing favorable terms.

But in practice, it’s more nuanced.

Many doctors earn through a mix of:

- PAYG income

- contractor or locum work

- private billing

- multiple entities or clinics

Lenders don’t always treat these equally.

Some income is discounted. Some requires history. Some is averaged conservatively.

At the same time, lending conditions remain relatively tight. The Reserve Bank has noted that serviceability buffers and lending standards are still stricter than pre-pandemic levels, even as credit growth increases, which is why working with specialist mortgage and investment property finance services can be so valuable for doctors.

So while doctors often have higher potential borrowing capacity, accessing it properly requires the right structure.

How lenders assess borrowing capacity for doctors

This is where most confusion happens.

Because what you earn and what you can borrow are not always the same. This assessment also determines the loan terms and features available to doctors, such as interest rates, repayment structures, and flexible options that can help manage repayments during periods of fluctuating income.

Income assessment isn’t always straightforward

Depending on your situation, lenders may:

- Shade contractor income (e.g. use 80%)

- Average income over 1–2 years

- Require financials for private practice

- Exclude certain bonuses or irregular income

- Assess income differently based on your personal circumstances

This can significantly impact borrowing power if not structured properly.

Serviceability buffers reduce usable borrowing

Even with strong income, lenders apply buffers.

Typically:

- Interest rates are assessed above actual rates

- Living expenses are benchmarked conservatively

- Existing debts reduce borrowing capacity

Serviceability calculations can also affect tax liabilities, depending on how loans are structured.

This means your “on-paper” affordability is often lower than expected.

Existing property and debt structure matters

If you already own property, your structure plays a big role.

Things like:

- loan splits

- offset accounts

- rental income assumptions

…can either support or limit your next purchase.

The value of your property and how you manage your property portfolio directly affect your ability to leverage equity for future investments. This is why we always recommend starting with a clear position using tools like our borrowing calculators, then refining it based on your actual structure.

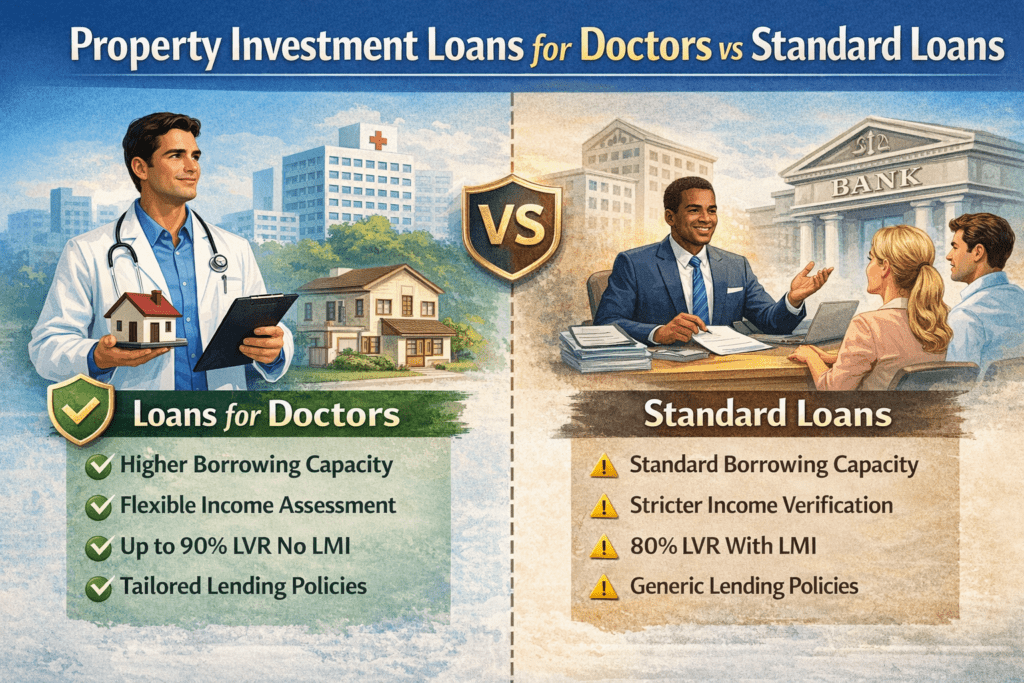

What makes a “doctor-friendly” investment loan

Not all loans are equal.

Some lenders offer more flexible policies for medical professionals, but the real value comes from how the loan is structured. Tailored solutions and specialist expertise are crucial, as doctors often require loan structures that address their unique income streams and investment goals. Working with a mortgage broker who provides tailored loan options can make the process much smoother and more efficient for doctors.

Higher LVR options without lenders mortgage insurance (LMI)

Some lenders allow doctors to borrow up to 90% without paying LMI.

This can:

- reduce upfront costs

- preserve cash for future investments

- accelerate entry into the market

But it’s not always the right move. It depends on your broader strategy.

Flexible income recognition

Certain lenders are more comfortable with:

- contractor income

- short-term employment history

- multiple income streams

Opting for a flexible loan can help doctors manage variable income streams more effectively by providing adjustable repayment options and greater control over loan terms.

Choosing the right lender can materially impact borrowing capacity.

Loan structuring for scalability

This is where most people miss the opportunity.

Properly structuring loans can help doctors minimise tax liabilities and provide greater financial control, making it easier to manage repayments and adapt to career changes.

A good structure considers:

- how you’ll build and manage a diversified property portfolio for long-term success

- future equity access

- ability to refinance

- preservation of borrowing capacity

Not just approval for one property.

The biggest mistakes doctors make with investment property loans

These are common. And costly. Making the right decisions at this stage can make all the difference in your long-term investment success.

Treating loan approval as the goal

Approval is just the starting point.

The real question is: Does this structure allow you to buy again? Considering your future loan repayments is essential for sustainable investment growth, as manageable repayments help ensure you can continue building your property portfolio over time.

Using a generic broker unfamiliar with medical income

Working with a team of specialist property investment finance experts who understand medical professionals can make a significant difference to your long-term results.

Not all brokers understand:

- how to present complex income

- which lenders are more flexible

- how to structure for long-term growth

- the unique benefits and requirements of home loans for doctors, such as waived LMI and discounted rates

That gap can reduce borrowing power significantly.

Not planning for future rate changes

Rates don’t need to rise dramatically to impact borrowing.

Even small increases can:

- reduce serviceability

- increase holding costs

- slow down portfolio growth

Seeking discounted interest rates and competitive rates can help doctors manage loan costs even as rates fluctuate. Some lenders offer competitive interest rates specifically for doctors, providing an advantage in keeping mortgage payments lower and supporting better financial planning.

This is why buffers matter.

Overcommitting on the first purchase

It’s tempting to maximise borrowing immediately.

But that can:

- reduce flexibility

- increase risk

- limit future opportunities

Overcommitting may also restrict your ability to make extra repayments, which can slow down how quickly you pay off your loan.

Sometimes a slightly more conservative first step leads to faster overall growth.

How to structure investment property loans for long-term portfolio growth

This is where the real advantage sits.

Because the goal isn’t just to buy one property.

It’s to build a portfolio. Structuring your investment property loans for doctors effectively not only opens up more investment opportunities, but also helps you build a robust investment portfolio for long-term growth. Ongoing support is crucial in managing your portfolio and ensuring you can take advantage of future opportunities as they arise.

Step 1: Define your borrowing strategy

Before looking at property, we map:

- borrowing capacity

- income stability

- buffer requirements

Incorporating financial planning at this stage can help doctors achieve better financial outcomes, such as improved cash flow, asset growth, and long-term wealth.

This is where our wealth advisory approach comes in.

Step 2: Choose the right lender for your situation

Different lenders treat medical income differently. Financial institutions have varying policies for assessing medical professionals, with some offering more favorable terms or specialized programs for doctors based on their unique financial profiles, so partnering with Australia’s leading property investment firm helps you navigate the right options.

We assess:

- income recognition policies

- flexibility for future refinancing

- long-term fit, not just initial approval

Step 3: Structure loans for flexibility

Staying across broader property investment trends and strategies in Australia can help ensure your loan structure supports how the market is evolving.

This includes:

- splitting loans where appropriate

- using offset accounts effectively

- planning for future equity access

- selecting loan features that provide flexibility for future changes, such as repayment options or redraw facilities, which can help doctors manage repayments during career transitions or periods of fluctuating income

Step 4: Align loan structure with property strategy

This is where most people fall short.

Loan structure should support:

- your next purchase

- your cash flow

- your long-term goals

- ensuring your loan structure aligns with your investment goals

Not just your current situation.

Tax and legal considerations for doctors investing in property

As a medical professional, property investment offers a powerful way to build long-term wealth and diversify your income. However, to truly maximise the benefits and protect your financial position, it’s essential to understand the tax and legal considerations that come with investing in real estate.

Why timing still matters (but not the way most people think)

A lot of doctors wait for the “perfect” time.

But the market doesn’t always cooperate.

Australia’s population continues to grow strongly, while housing supply is still catching up. Over time, this imbalance supports demand for well-located property.

By analyzing market trends and understanding the property market, doctors can identify the best investment opportunities and areas with strong growth potential. Exploring smart property investment strategies in Australia can also help clarify which approach best fits your risk profile and income. It’s also worth considering commercial property as part of a diversified investment strategy, as it can offer higher rental yields and more stable income streams.

So the better question isn’t: Is this the perfect time?

It’s: Is this structured properly for my situation?

How this fits into your broader property strategy

Loans don’t exist in isolation. They’re just one part of a broader plan that a dedicated expert guide to property investment can help you design and implement.

They connect directly to how you source and secure the right properties with a residential buyer’s agency:

- property selection

- tax positioning

- portfolio growth

- using specialist property construction services where appropriate to add value to your assets

- seeking tax advice to maximize tax benefits and improve cash flow as part of your property strategy

If you haven’t already, our guide on property investment advisors for doctors breaks down how strategy ties everything together.

Book a call if you want your borrowing structured properly from the start

If you’re a doctor thinking about investing, you probably already know your income gives you an advantage.

The question is whether you’re using it properly.

At Liviti, we help you:

- understand your real borrowing capacity

- structure your loans for flexibility

- choose lenders strategically

- align finance with long-term portfolio growth

- handle all the paperwork involved in securing your investment property loan

If you’re ready to move forward with clarity, book a call with us or reserve a spot at one of our live property investment webinars.

Because the goal isn’t just to get a loan approved.

It’s to build a structure that lets you keep investing.