You May Also Like:

- Investment Property Loans For Doctors: How To Maximise Borrowing And Build A Scalable Portfolio

- Property Investment Advisors Sydney: What They Actually Do And How To Choose The Right One

- Smsf Property Investment Strategy: How To Build Long-Term Wealth With Super

We’ve worked with doctors earning well into six figures who still felt stuck. Not because they lacked capital. Because nothing felt clear enough to act on. Making the right decisions in the early stages of a doctor’s financial journey is crucial to set a strong foundation for future property investment success. A property investment company like Liviti can help doctors build a tailored portfolio aligned with their financial goals.

TL;DR

Property investment advisors for doctors focus on structuring finance around complex and evolving income, aligning property decisions with tax efficiency, and building portfolios that scale over time. With lending still relatively tight and housing demand continuing to outpace supply, a clear, integrated strategy matters more than ever. For doctors, the goal isn’t just to invest. It’s to build a portfolio that works around your career, income trajectory, and limited time. Property investment advisors for doctors provide specialised guidance based on unique career structures.

Why property investing feels harder for doctors than it should

On paper, it shouldn’t be this complicated.

High income. Strong borrowing potential. Stable career.

But in reality, most doctors we speak to are overthinking, delaying, or stuck in a loop of “almost ready.”

Here’s what we actually see:

- You earn well, but income feels inconsistent

- You don’t have time to research properly

- Every decision feels high-stakes

- You’re unsure how to structure things long-term

To avoid analysis paralysis, it’s important for doctors to determine their investment goals, financial capacity, and risk tolerance early on. This helps clarify objectives and makes it easier to move forward with property investment decisions.

And the frustrating part?

You’re not wrong to feel that way.

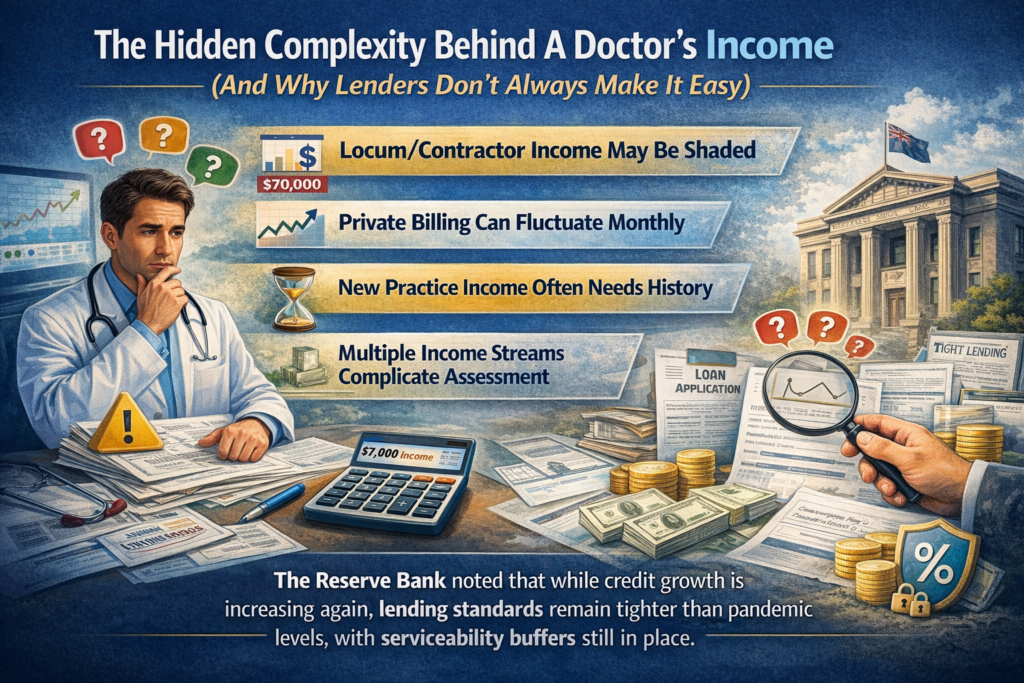

The hidden complexity behind a doctor’s income (and why lenders don’t always make it easy)

This is where generic advice breaks down quickly.

Medical income isn’t always clean or predictable from a lender’s perspective.

For example:

- Locum or contractor income may be shaded

- Private billing can fluctuate month to month

- New practice income often needs history

- Multiple income streams complicate assessment

At the same time, lending conditions are still cautious.

The Reserve Bank noted that while credit growth is increasing again, lending standards remain tighter than pre-pandemic levels, with serviceability buffers still in place.

So even with a strong income, structure becomes critical.

This is why we always start with a clear borrowing strategy using tools like our borrowing power calculator, then refine it based on your actual income profile. Choosing the right loan structure and understanding how interest rates affect your repayments are essential, as the total cost of property investment for doctors can be significantly impacted by loan features and interest over time, and partnering with an expert guide to property investment can help you make these decisions with confidence.

What property investment advisors for doctors actually do differently

Doctors don’t need more information.

They need advice that fits how their income, time, and career actually work. A tailored service from property investment advisors for doctors provides comprehensive support in property research, acquisition, management, and investment strategy, addressing the unique needs of medical professionals.

We structure your borrowing around where your career is going, not just where it is today

A junior doctor and a specialist may both be “high income,” but their trajectories are completely different.

We look at:

- expected income growth

- stability of income streams

- upcoming transitions (fellowship, private practice)

Because buying too cautiously early can slow you down just as much as overextending.

A dedicated team of property investment advisors, including financial specialists and mortgage brokers, can help doctors navigate the complexities of borrowing and career transitions.

We build a strategy that respects your time (because you don’t have much of it)

Most doctors don’t have time to:

- analyse suburbs deeply

- compare dozens of properties

- track market cycles

And realistically, you shouldn’t need to. With the right support, you can focus on your medical career while still building a diverse property portfolio for long-term success.

Instead of overwhelming you with options, we narrow it down to assets that:

- fit your strategy

- align with your borrowing

- support long-term growth

- are in the right location to maximize growth and rental demand.

That’s how we reduce decision fatigue without cutting corners.

We align property decisions with your tax position

This is one of the biggest missed opportunities.

Doctors often face time constraints and complex income structures, making a property investment company essential for strategic planning. Using tax effective strategies can help maximize returns for doctors by optimizing deductions and overall investment efficiency.

We consider:

- how deductions affect real cash flow

- when growth vs yield makes more sense

- how ownership structure impacts long-term outcomes

- the tax benefits available through property investment, such as depreciation and mortgage interest deductions

This is where our wealth advisory approach becomes important, because property decisions don’t exist in isolation.

We plan beyond your first property from day one

This is the difference that most people feel, even if they can’t explain it.

Instead of asking: “What should you buy next?”

We ask: “What does property three look like?”

That changes: Before making any decisions, we focus on developing a clear property strategy to guide the building of a successful investment portfolio over time.

- how we structure loans

- what assets we prioritise

- how we time purchases

And it’s why many of our clients avoid getting stuck after property one.

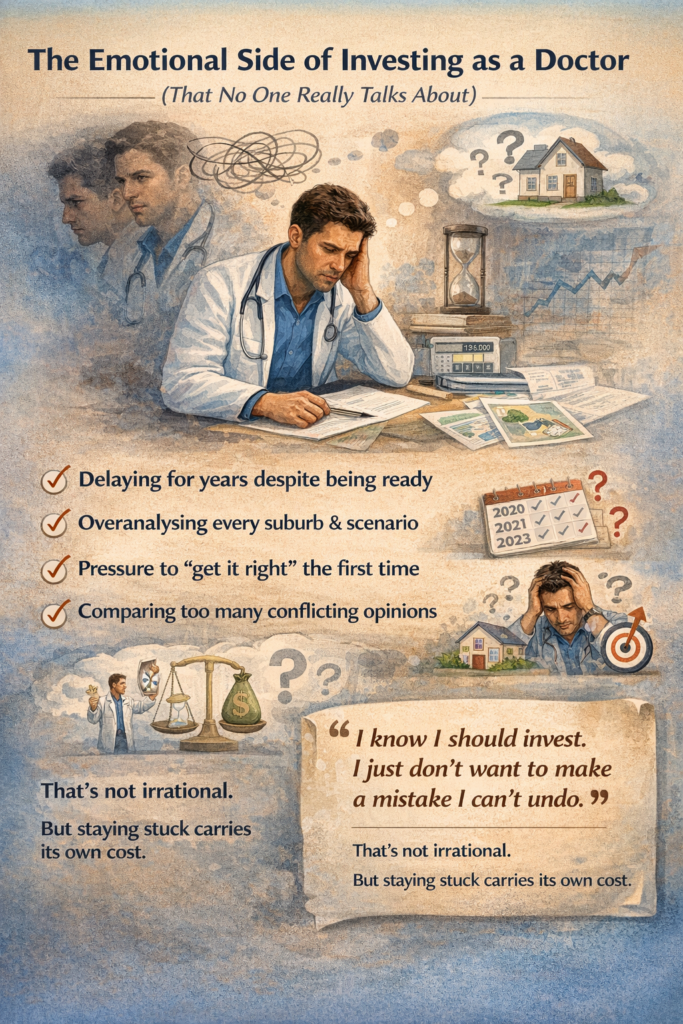

The emotional side of investing as a doctor (that no one really talks about)

This matters more than most people expect.

Because the biggest blockers aren’t always financial.

They’re psychological.

Many doctors face similar emotional hurdles when considering property investment, which is why having an experienced property investment finance team behind you can make it easier to move from uncertainty to action.

We’ve seen:

- Doctors delaying for years despite being ready

- Overanalysing every suburb and scenario

- Feeling pressure to “get it right” the first time

- Comparing too many conflicting opinions

One conversation that stuck with us was a specialist who said:

“I know I should invest. I just don’t want to make a mistake I can’t undo.”

That’s not irrational.

But staying stuck carries its own cost.

What the market is doing right now (and why waiting isn’t always safer)

Right now, housing demand is still being driven by population growth and supply constraints.

Australia’s population grew by over 420,000 people in a single year, with net overseas migration exceeding 300,000. At the same time, housing supply is forecast to fall short of new household formation over the coming years.

That imbalance matters, as shown by recent data on national median home values hitting record levels.

Because it supports:

- price stability over time

- rental demand

- long-term growth potential

It doesn’t mean you rush.

But it does mean waiting without a plan can quietly reduce your options. Taking proactive steps now is essential to achieve your property investment objectives efficiently and effectively.

The biggest mistakes we see doctors make when investing

These aren’t obvious at first. That’s why they’re common. The right property investment advisor can assist doctors in navigating these pitfalls, providing guidance and support to help avoid costly mistakes.

Relying on income instead of structure

High income helps.

But without structure, it can still lead to:

- stalled portfolios

- inefficient tax outcomes

- missed opportunities

- missed opportunities to generate more income through positive gearing or strategic property selection.

Buying something “easy” instead of something strategic

It’s tempting to buy something familiar or convenient.

But convenience doesn’t always align with:

- growth potential

- borrowing impact

- long-term positioning

Strategic property selection, guided by experienced property investment advisors for doctors, can unlock greater long-term benefits such as wealth building, passive income, tax advantages, and portfolio diversification—advantages that are especially important for medical professionals seeking financial stability and growth. Exploring smart property investment strategies in Australia can further clarify which approaches best align with your goals and risk tolerance.

Not thinking beyond property one

This is the most common issue.

Without planning ahead:

- borrowing gets constrained

- equity isn’t optimised

- momentum slows

Actively managing your property portfolio is crucial to maintain momentum and optimize returns as your investments grow, and working with Australia’s leading property investment firm can give you access to the research, financing structures, and support needed to scale effectively.

If you haven’t already, our guide on property investment advisors Sydney breaks this down further from a broader perspective.

How to choose the right property investment advisor as a doctor

This decision shapes everything that follows.

Working with independent financial advisers who possess specialized expertise in property investment for doctors ensures you receive unbiased advice and strategic guidance, helping you achieve the best outcomes for your financial future.

Look for someone who understands medical income

Not all advisors do.

You want someone who knows how to:

- present your income to lenders

- structure around variability

- plan for future growth

- integrate your business and personal financial goals for a holistic approach

Make sure strategy comes before property

If the conversation starts with listings, pause.

It should start with:

- your income structure

- your borrowing capacity

- your long-term goals

- your tailored financial plans

Ask how they help you scale

Anyone can help with one property.

Fewer can help you:

- preserve borrowing capacity

- sequence purchases

- build momentum

- access to exclusive property opportunities and resources

Choose a process that connects everything

At Liviti, we integrate comprehensive guidance, from property selection and finance structuring through to smart property investment strategies tailored to Australian investors:

- wealth advisory

- mortgage broker services

- tools like our borrowing calculators

- insights across our property investment blog

Our integrated approach also includes developing tailored investment strategies for doctors, ensuring your property investments align with your financial goals and risk profile.

Because disconnected advice slows everything down.

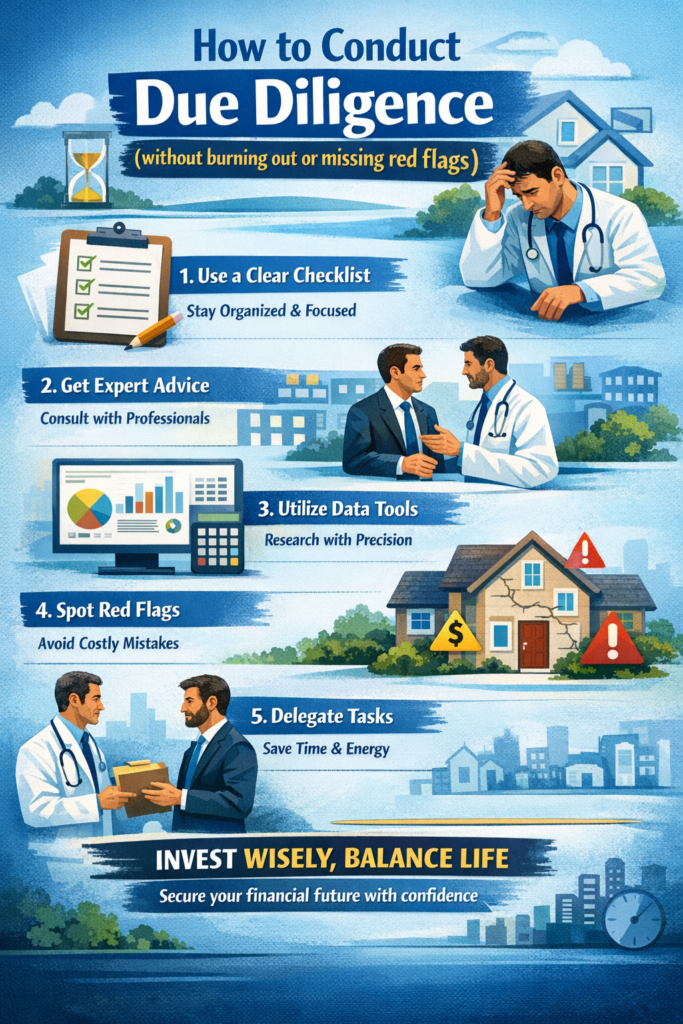

How to conduct due diligence (without burning out or missing red flags)

For doctors, conducting due diligence on an investment property is one of the most important steps in securing your financial future—yet it’s also one of the most overwhelming. With a demanding medical career, it’s easy to feel like you don’t have the time or energy to dig into the details of every residential property or commercial property you consider. But skipping this step can put your investment, and ultimately your financial security, at risk.

So, how can you approach due diligence in real estate without burning out or missing critical red flags?

1. Start with a clear checklist. Whether you’re investing in residential or commercial property, having a structured due diligence checklist helps you stay focused and efficient. This should cover everything from title searches and zoning to building inspections, rental history, and local market trends. For medical professionals, a checklist ensures you don’t overlook key details, even when time is tight.

2. Leverage specialist advice. You don’t have to do it all yourself. Engaging a property advisor, buyer’s agent, or other real estate professionals can help you identify risks and opportunities you might miss on your own. These experts can handle much of the legwork, allowing you to focus on your medical practice while still making informed investment decisions, and educational resources such as Liviti property investment webinars can further support your understanding without demanding too much of your time.

3. Use data-driven tools. Take advantage of technology and online resources to streamline your research. Property reports, suburb profiles, and cash flow calculators can quickly highlight whether an investment property aligns with your financial goals and risk profile. This approach saves time and helps you make decisions based on facts, not just gut feeling, especially when assessing specific risks like apartment oversupply in key markets.

4. Watch for common red flags. Some warning signs are easy to miss if you’re not looking for them:

- Unusual contract terms

- Poor building condition or hidden defects

- Overly optimistic rental estimates

- Lack of comparable sales in the area

- High vacancy rates or declining local demand

Spotting these early can save you from costly mistakes and protect your financial wellbeing.

5. Delegate where possible. As a doctor, your time is valuable. Don’t hesitate to delegate tasks to trusted professionals who understand both real estate and the unique challenges of investing as a medical professional. This not only reduces your workload but also ensures your due diligence is thorough and effective.

By approaching due diligence with a clear plan and the right support, you can confidently invest in property—knowing you’re protecting your financial future without sacrificing your career or personal life, whether you’re buying established properties or engaging specialist property construction services to develop new assets.

Book a call when you want a strategy that actually fits your career

If you’re a doctor, you don’t need convincing that property matters.

You need a plan that fits your income, your time, and your trajectory.

At Liviti, we help you:

- understand your real borrowing position

- structure your loans properly

- choose assets that support long-term growth

- map your next moves clearly

If you’re ready to move from “almost ready” to actually moving, book a call with us.

Because the goal isn’t just to invest.

It’s to build a portfolio that works around your career, not against it. Property investment advisors for doctors play a crucial role in supporting wealth creation, guiding effective retirement planning, and helping you achieve financial independence for a secure retirement.