A property investment company is a specialist advisory firm that helps you build a property portfolio aligned with your income, tax position, and long-term goals. Here is what that means for you in practice:

- They work for buyers, not sellers

- They cover strategy, lending, acquisition, and tax

- They access off-market deals the public never sees

- They reduce expensive first-purchase mistakes

If you have been managing your portfolio alone, or have never invested before and want to get it right from the start, what follows covers exactly what separates a credible firm from one that just charges you for something a real estate agent would do anyway.

TL;DR

A property investment company provides end-to-end advisory covering portfolio strategy, finance structuring, and property acquisition on your behalf. The best firms assign specialists to each phase of the process rather than one generalist doing everything. For professionals earning $200,000 or more, engaging a dedicated property investment company consistently outperforms self-directed investing because every decision, from loan structure to suburb selection, is made with your full financial picture in front of the people making the recommendation.

What does an investment property company actually do?

Most people assume these firms just find properties. They do considerably more than that, and the distinction matters.

The role of a property investment company spans four main areas: portfolio strategy, finance structuring, property acquisition, and in some cases construction management. Each phase ideally involves dedicated specialists rather than one adviser wearing multiple hats.

Strategy comes first. A good firm maps your income, existing assets, liabilities, and tax situation before discussing a single suburb. They model scenarios: what you can borrow now, what your debt looks like in three years, and how each acquisition changes your borrowing capacity for the next purchase.

Finance follows. Lenders assess income differently depending on whether you are a salaried employee, a business owner, or a contractor earning variable income. A mortgage broker inside the same firm coordinates your lending structure directly with your investment strategy, so the two do not work against each other.

Acquisition comes after strategy and finance are locked in. The firm identifies properties aligned with your brief and runs independent assessment across yield, vacancy risk, comparable sales, and supply dynamics. Many firms also access properties that never reach public listing portals.

How is a property investment advisor different from a real estate agent?

This distinction matters more than most buyers realise, usually right after they get it wrong.

A real estate agent is legally required to act in the interests of the vendor. Their fee comes from the seller. A property investment advisor works exclusively for the buyer and is paid by them.

In practice, that creates very different incentives. An agent wants a deal done at the highest price. An advisor wants the right deal done at the right price. These are not always the same thing, and the gap usually shows up months after settlement.

Property investment advisors in Sydney and other capital cities also bring expertise that most real estate agents are not trained or required to have: income assessment for lending, tax implications of structure choices, portfolio sequencing across multiple assets, and long-term growth analysis informed by proprietary data.

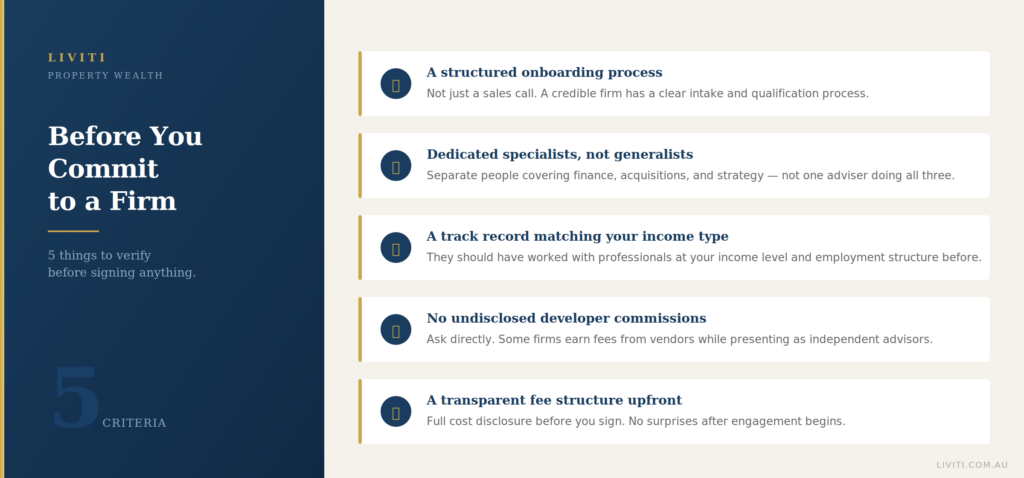

What should you look for in an investment property company?

The quality gap between firms in this space is real. Here is how to tell a credible one from a mediocre one before you commit to anything.

When evaluating a property investment company, look for:

- A structured onboarding process, not just a sales conversation

- Specialists in finance, acquisitions, and strategy

- A track record with your income type and investment profile

- No undisclosed developer relationships or referral commissions

- A transparent fee structure provided before you sign anything

Ask directly whether the firm earns any referral fees or payments from developers or property vendors. Some firms present themselves as independent advisors while taking commissions on the properties they recommend. That arrangement is not independent advice, regardless of what it is called.

How can property investment advisors in Sydney help doctors and high-income earners?

High income creates specific opportunities in property. It also creates specific complexity that most generalist advisors are not equipped to handle well.

Investment property for doctors is assessed differently by most lenders, particularly for professionals on variable contracts, locum arrangements, or income that includes overtime loading. Specialist property investment advisors for doctors know which lenders assess these income types most favourably, and how to structure borrowing across multiple properties without triggering unnecessary restrictions.

From a tax perspective, each negatively geared investment property generates deductions against employment income, reducing the tax you pay at the top marginal rate. According to the Australian Taxation Office, capital gains on properties held longer than 12 months attract a 50% discount, which significantly changes the after-tax return calculation for long-hold investors.

For dual-income households with equity sitting in offset accounts, a property investment strategy for doctors or other high-income professionals can redirect that idle equity into assets that generate both rental income and tax deductions from day one.

When is the right time to work with a property investment consultant?

The most common answer from our clients is earlier than they originally thought.

Most investors who engage a property investment consultant do so after buying their first property alone and realising they structured it incorrectly, paid too much, or chose a location that has underperformed. The first purchase is often the most expensive lesson.

The better time is before you buy anything, so that your first acquisition fits within a deliberate portfolio plan rather than being a standalone decision made in isolation. The structure of your first purchase directly affects your borrowing capacity for everything that follows.

It is also worth engaging a consultant when your financial situation changes materially. A significant equity event, a shift from salary to contractor income, or receiving an inheritance all create new opportunities that require a fresh assessment of what is possible.

Next steps

If you are a professional in Australia looking to start or grow a property portfolio, the first move is a strategy session, not a suburb search. Before looking at a single listing, get a clear picture of your borrowing capacity, tax position, and a realistic sequencing plan for the next two to three purchases.

Book a strategy session with the Liviti team to map what your next move should look like based on your actual numbers, not a generic template.