Property investment calculators give you the numbers behind the decisions before you make them, but not every calculator is relevant to every investor at every stage. Here is what actually matters:

- Borrowing power calculators set the ceiling before you look at anything

- Loan repayment calculators show weekly cash flow implications

- Capital gains calculators prevent tax surprises when you eventually sell

- Income annualisation tools are critical for non-standard income earners

The right calculator used at the wrong stage gives you numbers that feel useful but are not. What follows explains which property investment calculators belong at which point in your decision-making process.

TL;DR

Property investment calculators are tools for estimating outcomes, not guarantees. The most practically useful ones for investors starting out are the borrowing power calculator, which sets the boundary of what is possible, and the loan repayment calculator, which shows whether the ongoing cash flow is sustainable given your income and expenses. Advanced investors add the capital gains calculator when planning a sale, and the income annualisation calculator if their income is variable, contract-based, or received through a trust or company structure. Used in combination, these tools give a far more accurate picture than any single figure alone.

What is a borrowing power calculator and why does it matter for investors?

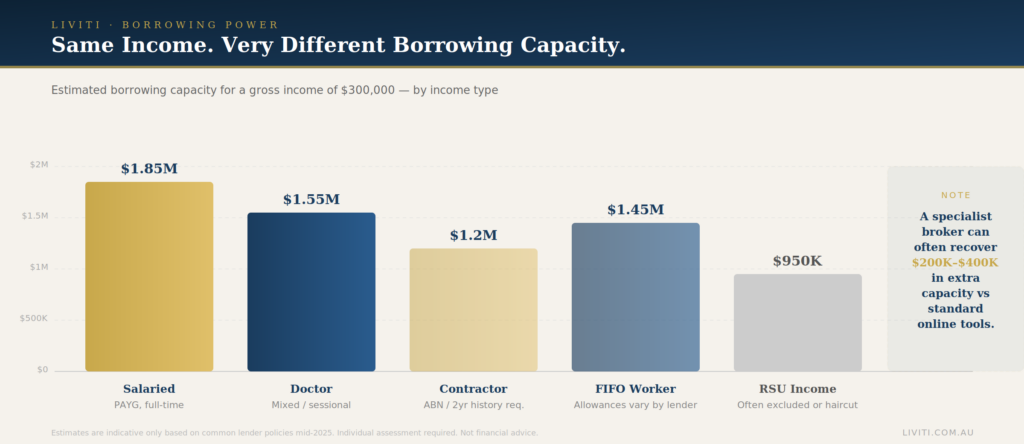

Your borrowing power is the upper limit of what lenders will approve based on your income, expenses, existing debts, and the type of property you are purchasing. A borrowing power calculator estimates that figure.

Most first-time investors start by looking at properties, then check whether they can afford one. The better approach is the reverse. Knowing your ceiling first means you search within a range that is actually achievable, rather than spending weeks investigating properties outside your approved limits.

The investment property borrowing power calculators on our platform typically ask for your gross income, any dependants, existing commitments such as car loans or credit cards, and your estimated deposit. They return an estimated borrowing capacity based on standard lender assessment criteria.

The important caveat: lenders assess income differently depending on how you earn it. A salaried professional at $300,000 will be assessed differently to a surgeon who earns the same amount through a combination of base salary, sessional income, and private billing. Standard online calculators use simplified assumptions. A specialist broker will give you a more accurate figure based on your actual income structure.

How does a property investment loan calculator help you compare financing options?

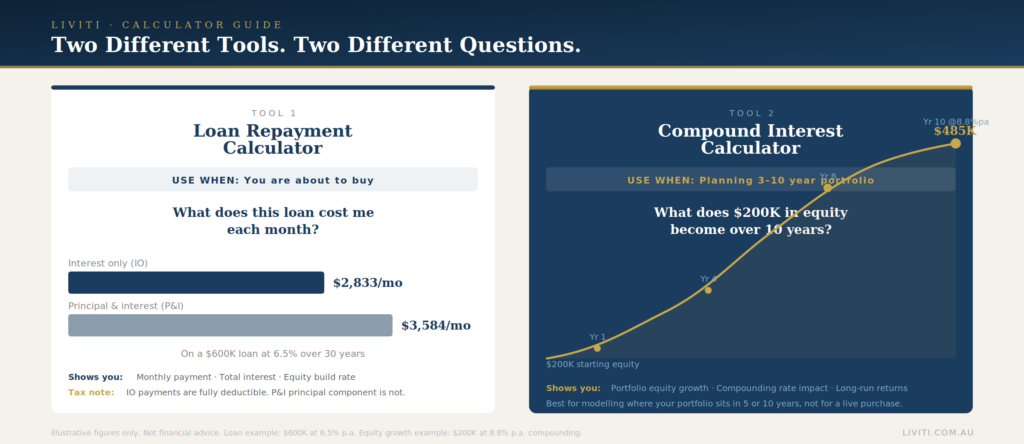

A property investment loan calculator answers a specific question: given a loan amount, interest rate, and loan term, what does the repayment look like and how much interest do you pay over time?

This matters when you are comparing loan structures. Interest-only repayments result in lower monthly outgoings and preserve cash flow, but they do not reduce the principal. Principal and interest repayments reduce your debt faster and cost less in total interest over the life of the loan, but they increase your monthly commitment.

For investors, the choice between interest-only and principal and interest is not just a cash flow question. It also affects your tax position, because the interest component of your repayment is tax-deductible as a rental property expense, while the principal component is not.

A property investment loan calculator lets you model both scenarios side by side. It shows you the monthly repayment difference, the total interest paid under each structure over five or ten years, and how quickly your equity position changes under each approach. Running this comparison before you commit to a loan structure is worth a few minutes of your time.

When should you use a compound interest calculator vs a loan repayment calculator?

These two tools answer different questions and they are often confused.

A loan repayment calculator tells you what you owe the bank each month, how much of each payment is interest versus principal reduction, and what the total interest cost looks like over the loan term.

A compound interest calculator shows you how an investment grows over time if the returns are reinvested or compounded. It is more relevant when modelling the long-term growth of equity in a property portfolio, or when comparing the return from a lump sum deposit versus ongoing contributions.

For most investors making an active purchase decision, the loan repayment calculator is the relevant tool. The compound interest calculator becomes useful when you are doing longer-range portfolio modelling: what does $200,000 in equity look like across three properties over ten years if growth compounds at a given annual rate?

Use the loan repayment calculator when you are about to buy. Use the compound interest calculator when you are planning the next three to five years of your portfolio.

Which property investment calculators should first-time investors use first?

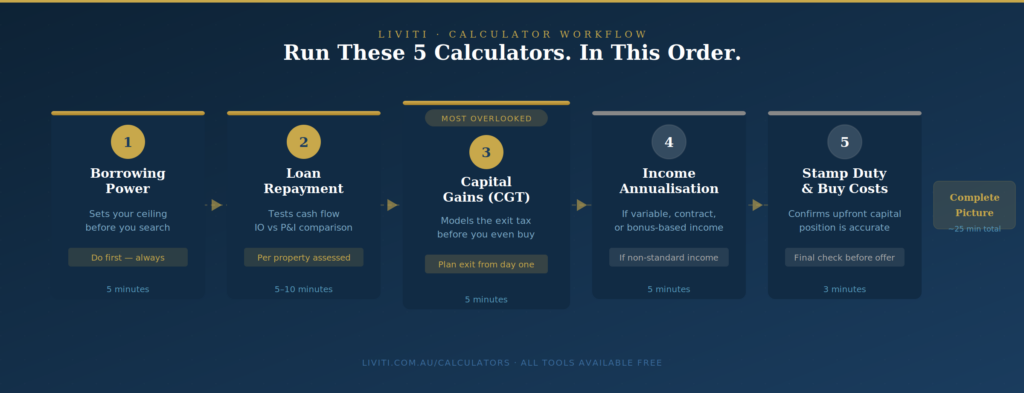

Start with borrowing power, then repayments, then tax.

A first-time investor should run their borrowing power calculation before looking at a single suburb or property. This takes five minutes and gives you a realistic boundary to work within. Most people overestimate or underestimate their actual borrowing capacity by a meaningful margin, and both errors are costly.

After borrowing power, run a loan repayment calculator on the properties you are seriously considering. This tells you what the weekly or monthly cash flow commitment looks like and whether the property is positively or negatively geared given current rental yields.

Then run a capital gains estimate for a five or ten year hold scenario. This is not about predicting growth. It is about understanding what a realistic exit looks like from a tax perspective so you can factor it into your decision from the start.

The income annualisation calculator is also relevant for first-time investors whose income includes overtime, bonuses, commission, or variable contract payments. Lenders in Australia annualise non-standard income differently, and knowing how a lender sees your income before you apply is substantially better than finding out after a decline.

How do these calculators work together to build a complete investment picture?

No single tool gives you everything. The value is in how they connect.

Start with borrowing power to set the ceiling. Run the loan repayment tool on properties at that ceiling to test cash flow sustainability. Use the capital gains calculator to model the exit. Add the income annualisation tool if your income is non-standard. Cross-reference with a stamp duty and buying costs calculator to ensure your upfront capital position is accurate.

What this process produces is a single, honest picture of the investment: what you can buy, what it costs you monthly, what the tax bill looks like when you sell, and whether the overall return justifies the capital deployed.

Run all five before you start seriously evaluating properties. Most investors who do this for the first time discover at least one assumption in their plan that was materially wrong. Catching that before you are under contract is the point.

Next steps

Run your borrowing power calculation first. It takes five minutes and sets the foundation for every other decision. Then work through the full set of property investment calculators on the Liviti calculators page to build a complete financial picture before you approach a lender or make an offer. If the results raise questions about structure, income assessment, or what the numbers mean for your specific situation, book a strategy session to work through it directly.