An SMSF property investment strategy is one of the most tax-advantaged ways to build long-term wealth in Australia, but it carries strict rules that most investors underestimate before they start. Here is what matters:

- SMSF property must pass the sole purpose test at all times

- You cannot live in or rent the property to related parties

- Borrowing requires a Limited Recourse Borrowing Arrangement

- Division 296 now creates additional tax for balances over $3 million

Getting the structure right before you sign anything is not optional. The compliance requirements are active and the consequences of getting them wrong affect your entire super balance, not just the property.

TL;DR

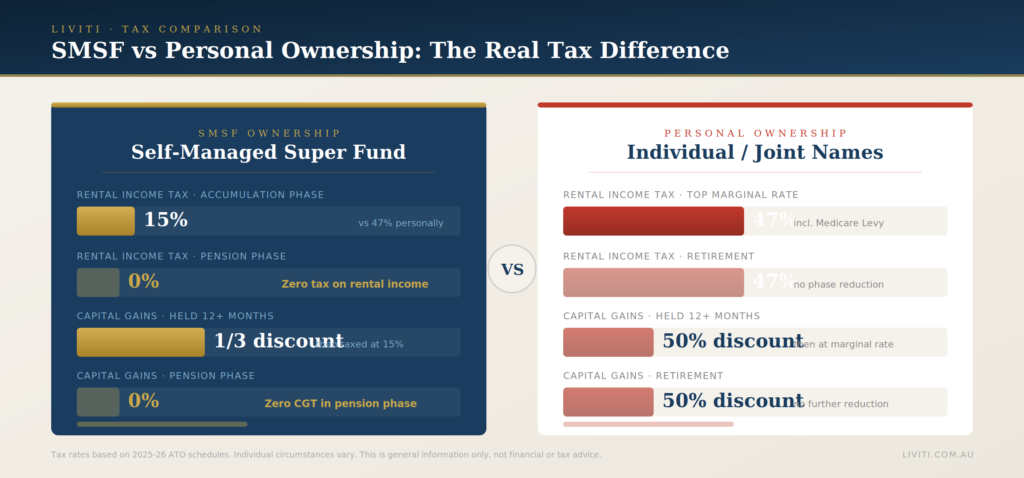

A self managed super fund property investment allows you to purchase residential or commercial property inside your superannuation environment, subject to strict Australian Taxation Office rules. The tax advantages are real: rental income is taxed at 15% during accumulation and 0% in pension phase, and capital gains attract a one-third discount for assets held over 12 months. The risk is equally real: liquidity constraints, concentration risk, and compliance obligations that require ongoing specialist oversight mean this is not a strategy for investors who want a set-and-forget approach.

What is an SMSF property investment strategy?

Understanding what this strategy actually involves is the foundation before any other question gets answered.

An SMSF property investment strategy involves using your self-managed superannuation fund to purchase property as a retirement asset. The fund owns the property, not you personally. All rental income flows into the fund. All expenses are paid from the fund. The goal is to build a retirement asset inside a tax-advantaged structure.

According to the Australian Taxation Office, as at December 2024, approximately 6% of all SMSF assets nationally were invested in residential property, representing around $58 billion. Commercial property held another 11.2% or approximately $110 billion.

The appeal is the tax treatment. During the accumulation phase, rental income earned inside an SMSF is taxed at 15%, compared to your personal marginal rate which may be as high as 47% including the Medicare Levy. In the pension phase, that rate drops to zero.

What are the rules around using a self-managed super fund for property?

The ATO has specific and non-negotiable requirements. These are not guidelines. They are conditions your fund must meet at all times.

The key rules for residential properties inside an SMSF are:

- Property cannot be used by you, your family, or related parties

- Property title must be in the name of the SMSF trustee

- Borrowing must use a correctly structured LRBA

- Personal loans or standard investment loans are not permitted

- The property must meet the sole purpose test at all times

For commercial property, the rules differ in one important way: your business can lease commercial property from your SMSF at market rent. This is one of the most commonly used strategies for small business owners who want their business premises inside their retirement structure.

From January 2025, SMSF trustees are also required to acknowledge in writing that they have received appropriate advice before proceeding with a property investment. The ATO’s scrutiny of Non-Arm’s Length Income provisions has intensified, making compliance documentation more important than at any previous point.

What are the key risks of buying investment property through an SMSF?

The tax advantages are attractive. The risks are just as real and often underweighted in the conversations investors have before they commit.

Liquidity risk is the most common trap. Property cannot be sold quickly if your fund needs cash to pay pension payments or meet other obligations. A fund that has most of its assets tied up in one property and faces an unexpected liquidity need has very limited options.

Concentration risk compounds this. Many SMSFs end up with one property representing 80% or more of the fund’s total assets. Diversification guidelines from the ATO require trustees to consider whether the investment strategy appropriately diversifies the fund’s assets. Holding one property and little else is a documented compliance risk.

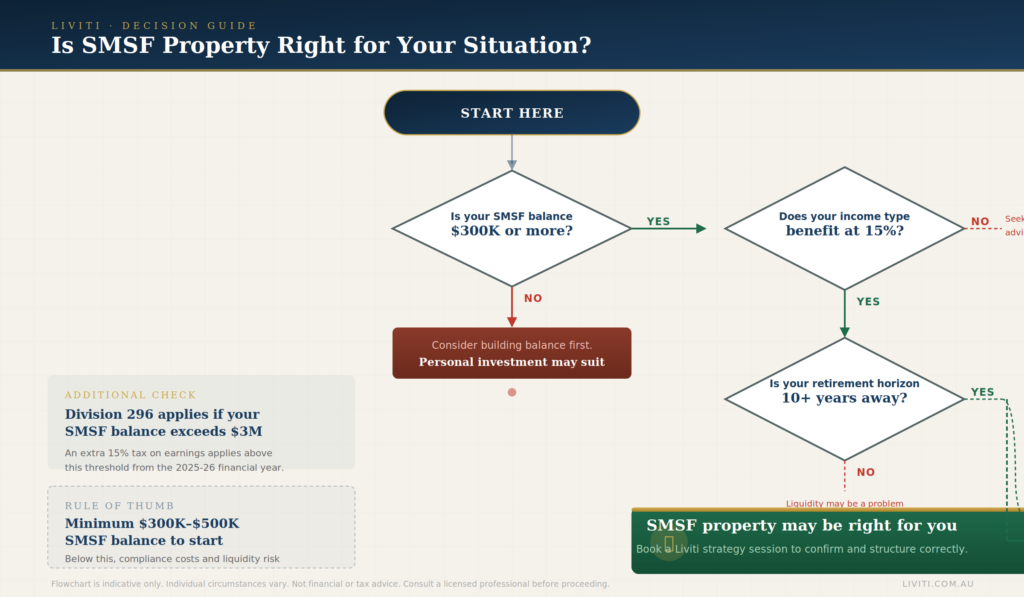

Division 296 is newer and affects high-balance investors specifically. Introduced for the 2025-26 financial year, it applies an additional 15% tax on earnings attributable to superannuation balances above $3 million. For investors with significant property equity inside their SMSF, this changes the return calculation materially.

[IMAGE: Risk matrix graphic for SMSF property investment]

SMSF loan rates have also shifted. As of mid-2025, SMSF loan rates averaged 6.8% to 7.3% variable, compared to standard investment loan rates. That spread affects cash flow projections for the fund, particularly in the early years of a borrowing arrangement.

How can a property investment company help you set up an SMSF strategy?

Setting up an SMSF correctly requires expertise across at least three disciplines: accounting, financial planning, and property advisory. Most individual advisers cover one of these well.

A property investment company that works with SMSF investors coordinates the lending structure, property selection, and acquisition process alongside your accountant and financial planner. The value is in the coordination, not just the property sourcing.

From a lending perspective, SMSF loans are assessed differently to personal investment loans. Lenders look at the fund’s overall financial position, not just the individual member’s income. Investment property advisors Sydney-based firms work with understand which lenders offer the most favourable SMSF loan terms for different fund profiles and investment types.

From an acquisition perspective, the property selected for an SMSF needs to meet specific criteria beyond normal investment assessment. Yield and liquidity matter more inside super than in a personally held portfolio, because the fund needs to be able to service the LRBA from rental income and contributions without requiring asset sales.

Is an SMSF investment property the right move for you?

Not for everyone. This is worth stating directly before anything else.

An SMSF property investment strategy works best when you have a sufficient fund balance to absorb the property without creating dangerous concentration, an income type that benefits specifically from the lower super tax rate, and a clear timeline that aligns with the fund’s liquidity requirements.

Most specialists suggest a minimum fund balance of $300,000 to $500,000 before property becomes an appropriate SMSF asset, simply to avoid the concentration problem. Below that level, the compliance costs and liquidity constraints tend to outweigh the tax advantages.

If you are a professional with a growing superannuation balance, existing property investment experience, and a business owner’s interest in using commercial premises strategically, the structure makes strong sense and is worth exploring in detail with a specialist team.

Next steps

Start with a conversation that covers your current SMSF balance, income structure, existing assets, and the timeline before you need the fund to start paying pension-phase income. Those four variables determine whether SMSF property is the right move for your situation or whether personal investment will serve you better.Speak to the Liviti team about whether an SMSF strategy fits your current position. The intake process takes one conversation and covers everything you need to make a considered decision.