Capital gains is the profit you make when you sell an investment property for more than you paid for it, and in Australia it is added to your taxable income for the year of sale and taxed at your marginal rate. Here is what the process involves:

- Capital gain is sale price minus your cost base

- Cost base includes purchase price, stamp duty, and improvements

- Assets held over 12 months attract a 50% CGT discount for individuals

- The gain is reported when the contract is signed, not at settlement

Understanding how to calculate capital gains on investment properties before you sell can change your decision on when to sell, how to structure your finances in the sale year, and how much to set aside for tax.

TL;DR

Capital gains tax on an investment property in Australia is calculated by subtracting your cost base from the sale price to get the gross capital gain, applying the 50% discount if you have held the asset for more than 12 months, then adding the remaining amount to your taxable income for that year. The Australian Taxation Office taxes the gain at your marginal income tax rate, which in 2025-26 ranges from 19% to 47% including the Medicare Levy. There is no separate CGT rate in Australia. It is part of your income tax.

What is capital gains tax and when does it apply to investment properties?

Most investors know that capital gains exist. Fewer understand exactly when the liability triggers and what events can change that timing.

Capital gains tax applies to investment properties when a CGT event occurs. For most property sales, that is the exchange of contracts. Not settlement.

According to the ATO, if contracts are exchanged on 4 June 2025 and settlement occurs on 6 July 2025, the gain must be reported in the financial year ending 30 June 2025, not the following year.

This timing distinction matters more than most investors realise. If you exchange contracts in June and settle in August, you may find yourself with a large tax liability in a year when you have not yet received the full sale proceeds.

CGT does not apply to your principal place of residence if you lived in the property for the entire period of ownership, did not use it to produce income, and the land is no more than two hectares. Partial exemptions apply for properties that were partially or temporarily used as rentals.

How do you calculate capital gains on an investment property?

The formula is straightforward. What complicates it is building the cost base accurately, because most investors underestimate what they can include.

The calculation works as follows:

- Capital gain = sale price minus cost base

- Cost base = purchase price + stamp duty + legal fees + improvements + selling costs

- If held over 12 months, apply the 50% CGT discount to the gross gain

- The discounted gain is added to your other taxable income for the year

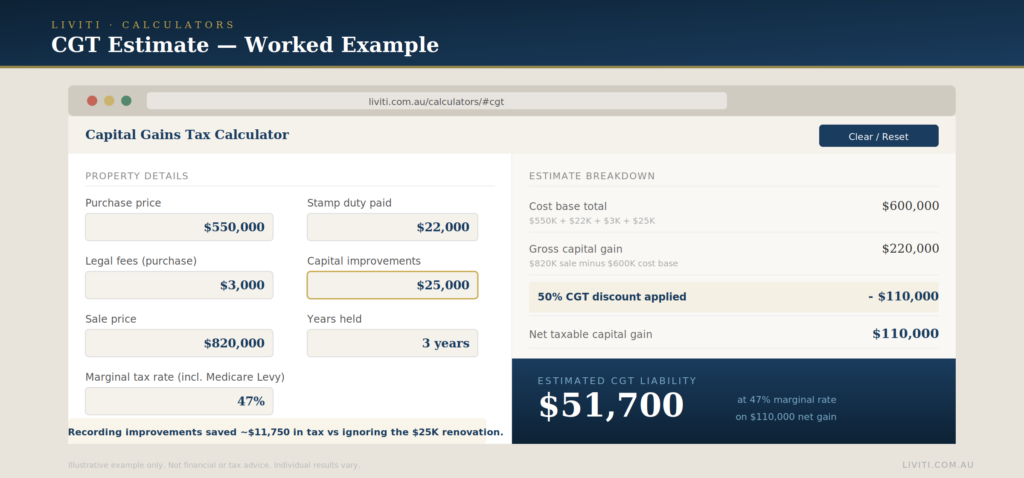

Here is a worked example. You purchase a property in Brisbane for $550,000. You pay $22,000 in stamp duty, $3,000 in legal fees on purchase, and spend $25,000 on a kitchen renovation. Your cost base is $600,000. You sell for $820,000. Gross capital gain is $220,000. You have owned the property for three years, so the 50% discount applies: $110,000 becomes your taxable capital gain.

At the 47% marginal rate including Medicare Levy, your CGT liability on that $110,000 is approximately $51,700. Notice how the renovation cost and buying expenses reduced the gain from $270,000 to $220,000. Keeping records of every capital improvement is worth the effort.

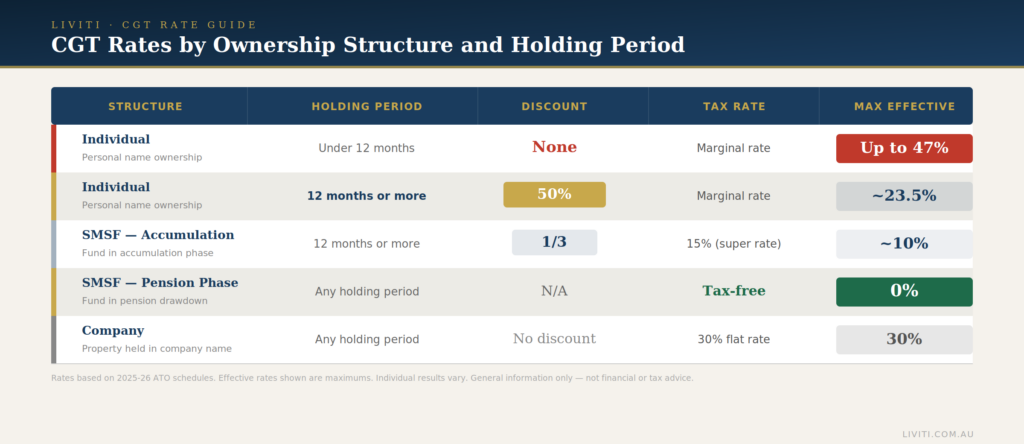

Does age affect when you have to pay capital gains tax?

Age itself does not change when CGT applies or how it is calculated. Super balances and fund type do.

If you hold an investment property inside an SMSF and the fund is in pension phase, the capital gain is taxed at 0%. If the fund is in accumulation phase and the property has been held for more than 12 months, the gain is reduced by one-third, then taxed at 15%.

For individuals, the marginal tax rate applied to the capital gain depends entirely on your total taxable income for that year, including the gain itself. Someone retiring with a low income in the year of sale pays a lower rate than someone who sells in a year when they are still earning full salary.

This is why the timing of a property sale relative to your income situation can save or cost significant money. Planning a sale for a year when your income is lower, or structuring the sale to straddle two financial years in some circumstances, can meaningfully reduce the total tax paid.

Can an investment property calculator help you estimate your CGT liability?

Yes, and using one before you make any sale decision is worth the few minutes it takes.

An investment property calculator for capital gains works by asking you to input your purchase price, cost base components, selling price, length of ownership, and current taxable income. It then estimates your gross gain, applies the 50% discount if applicable, and calculates the additional tax owed based on your marginal rate.

The Liviti calculators page includes tools to estimate your CGT liability, model your borrowing power for a replacement asset, and compare loan repayment scenarios side by side. Using multiple calculators together gives you a more complete picture of the financial outcome of any sale.

One thing most calculators will not do is account for your individual circumstances precisely: depreciation schedules, partial main residence exemptions, or timing strategies tied to your income situation. For those, you need a tax adviser who understands property specifically.

What should you do with your capital gains once you know the figure?

Knowing your estimated CGT liability is the starting point. What you do with that number is what determines the outcome.

Set aside the estimated tax before you deploy the sale proceeds into anything else. This sounds obvious and is frequently ignored. Running out of available funds to pay a tax bill because proceeds were already reinvested is a problem that a property investment calculator used early in the process prevents entirely.

Consider whether any capital losses elsewhere in your portfolio can be used to offset the gain. Capital losses can only be applied against capital gains, not ordinary income. If you have held underperforming shares or other assets, it may make sense to assess those positions before the end of the financial year in which you sell the property.

Review whether the proceeds are best redeployed into another investment property, superannuation, or held as a cash buffer depending on your current lending position and broader financial goals.

Next steps

Run the numbers before you list the property. Use the Liviti property investment calculators to estimate your CGT liability and model what the proceeds could support in your next purchase or structure. If the numbers raise more questions than they answer, that is the right time to book a strategy session and work through the specifics with a specialist.